A regression and classification problem to calculate the closing price of the NASDAQ composite index on a given day based on a series of domain-centric feature vectors. I compared two research papers based on the different methodologies used.

The two research papers compared are :

Stock Market Prediction by Using Artificial Neural Network

A Machine Learning Approach for Stock Price Prediction

There are five basic input vectors used in all papers predicting stock market prices.

• Open Price

• Low Price

• Volume

• High Price

• Adjusted Close Price

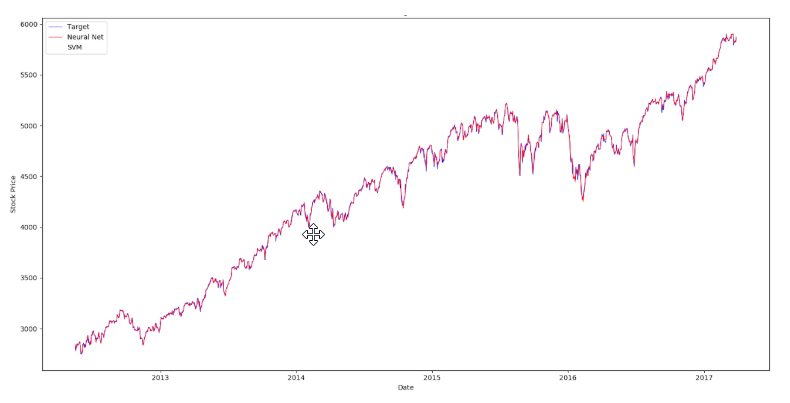

The output vector is the Close Price of the stock on a given day.

There are totally 1223 data points, each data point signifying the stock index from

3/29/2012 to 3/28/2017. The first paper used data points from 2012-2013, and our research

reproduction is based on a five year data pool.

Data source:

https://www.quandl.com/data/NASDAQOMX/COMP-NASDAQ-Composite-COMP

Neural Networks

SSVM

class sklearn.neural_network.MLPRegressor (solver='lbfgs', hidden_layer_sizes=10, shuffle=True, max_iter=150, random_state=1, momentum=0.75, alpha=0.4)

There are three solvers available in sci-kit learn out of which lfbgs has been used here. The

other parameters are quantified below.

Before fitting X and y, I must first normalize the input vectors in order to avoid local

optima.

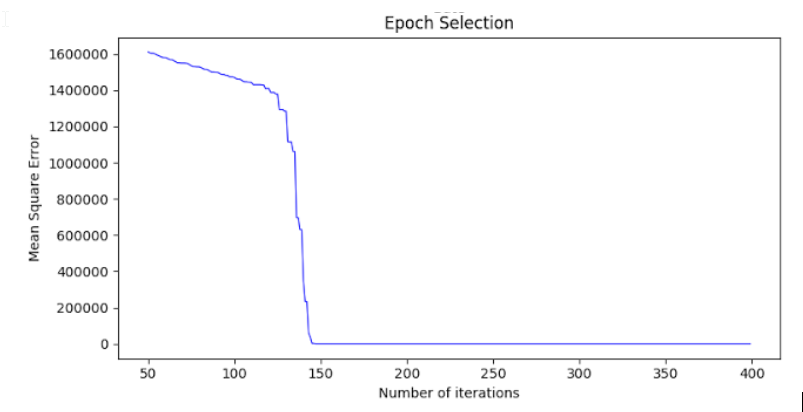

The epoch number (maximum iterations) was determined by running an iteration of the

MLP before a constant mean error was reached.

I reached a lower number of maximum iterations than the research paper due to a much

larger dataset.

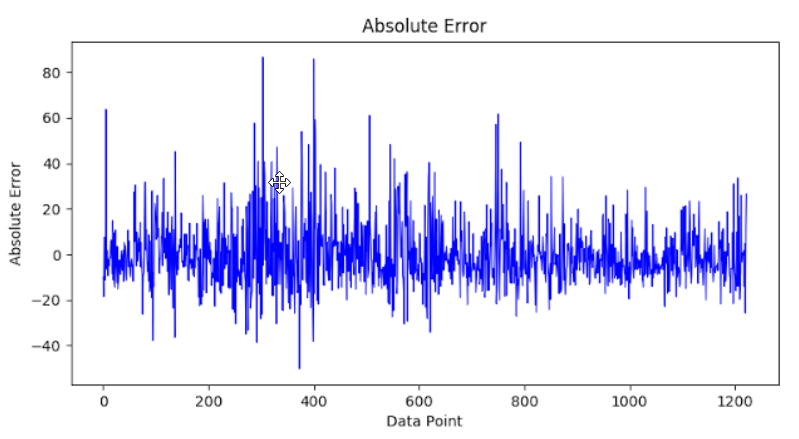

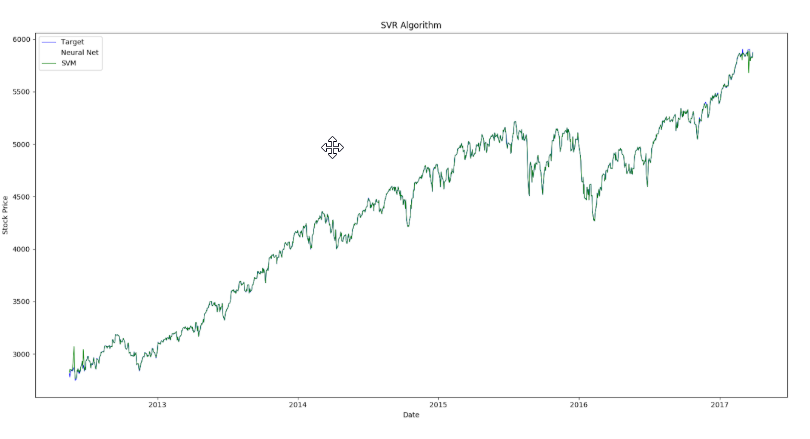

Using this epoch value, I can calculate the mean square error to compare accuracy with

the research paper. The authors have attained error in the range of -120 to +100. The mean

square error obtained by us is 210.01, and the error range is as follows.

The range of MSE is -40 to 80.

In conclusion, this paper was reproduced with almost identical results, resulting in an error

of approximately 0.2%.

The second paper employs Structured SVM on a very similar dataset, but with additional

feature vectors for classification. Since sci-kit learn does not support SSVM, a third party

library called pystruct was used. New features were introduced such as Daily Return in

order to transform the problem statement into a classification of positive return or

negative return.

The advantage of SSVM is that unlike traditional SVM, a graph structure can be used as

input. Each node of the graph is a company, and each edge denotes a collaboration

between two companies. The relationship between two companies who collaborate is

associative, and each company will see a profit if its partner company also sees a profit.

However, this assumption was not justified in the research paper, and further

reproducibility was hindered due to very vague methodologies used.

Therefore, I implement traditional SVM to our first research paper and compare results.

class sklearn.svm. SVR(C = 1000.0, epsilon= 0.1, cache_size=10000)

The parameters can be further tuned using the GridSearch algorithm.

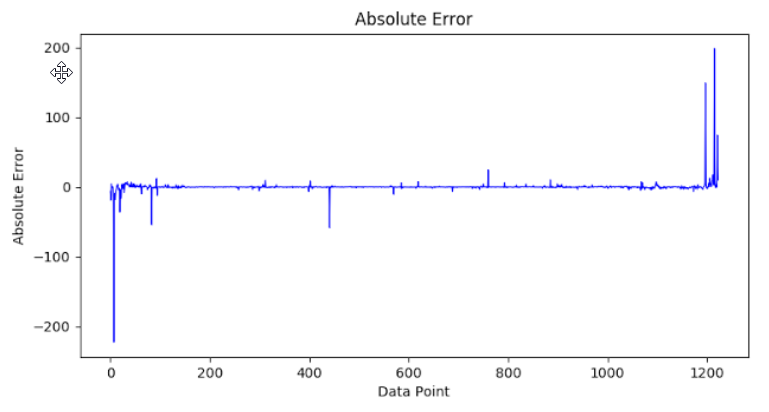

A mean square error of 106.94 was obtained, which proves the superiority of SVR over

neural networks in this problem.

SVR also requires regularized values as inputs and tuning of epsilon and C is very

important.

Further regression algorithms were also considered, such as Logistic regression, later discounted due to floating point feature vectors.